Monday, Apr 5, 2021 | 06:00 AM - 06:45 AM

Location: AV CORE

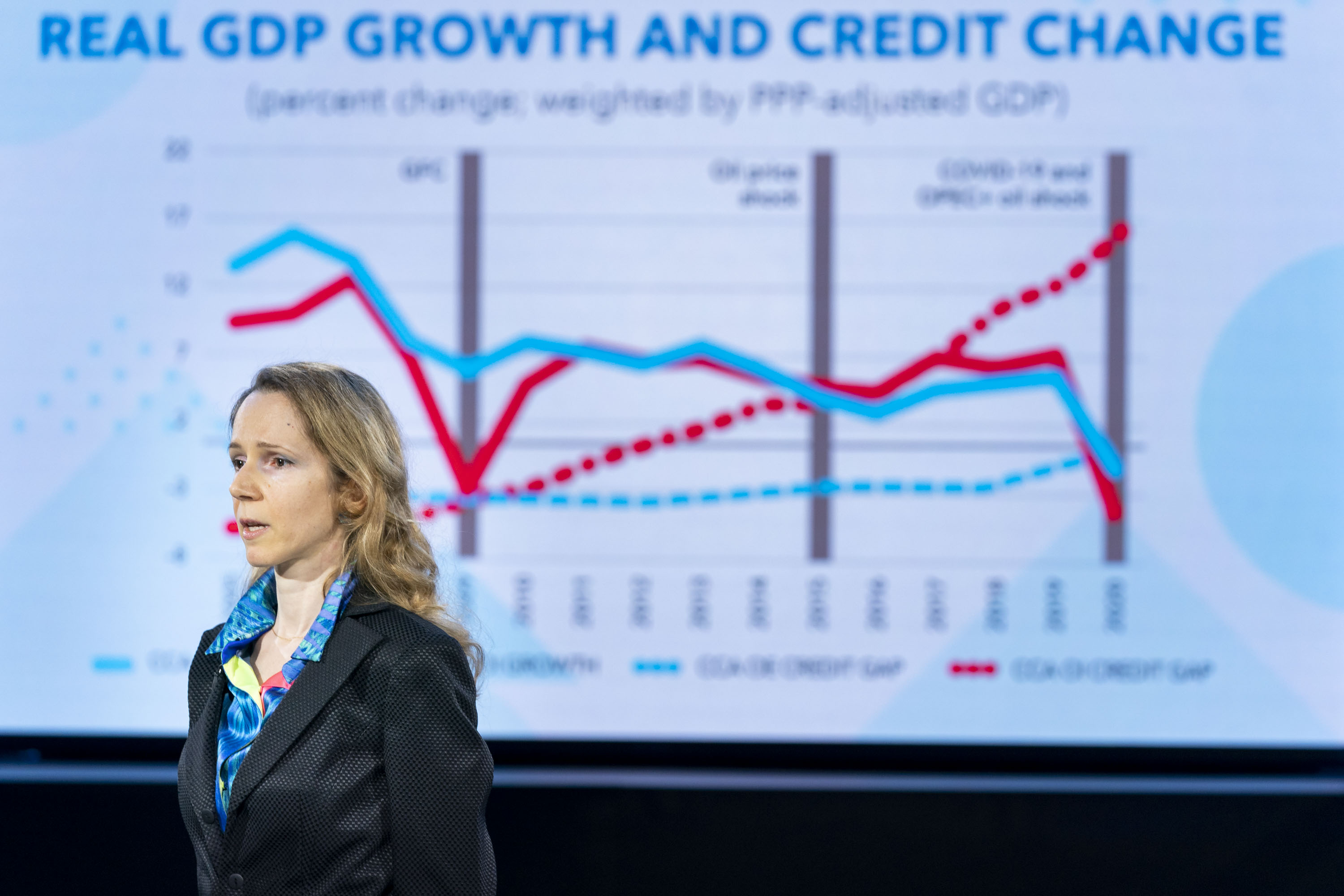

The strength of balance sheets is key to determining how well firms and households can weather the COVID crisis and how vigorously an economy can bounce back. Weak balance sheets, reflected for example by low liquidity or excessive leverage of non-financial corporates (NFC), limit NFCs’ capacity to cope with times of stress and may constrain future investment. In turn, poor economic conditions tend to leave their mark on balance sheets, as losses eat up equity buffers and cash-flow shortages lead to payment difficulties. Corporate sector vulnerabilities can also spill over to other sectors of the economy through a network of credit and ownership relationships. In this presentation we document the evolution of balance sheets in Europe during the pandemic and discuss the role of policy in shaping it. Using sectoral balance sheet data from the European Central Bank (ECB) through the third quarter of 2020, we observe that the patterns of previous crises have not been repeated, at least so far. We argue that this has much to do with the extraordinary nature of the policy response and explore what this could mean for the path ahead.

|

Estelle Liu European Department, IMF |

|

Karim Foda European Department, IMF |

|

lulia Teodoru Middle East and Central Asia Department, IMF |

The COVID-19 outbreak and the measures to contain the virus have caused severe disruptions to labor supply and demand worldwide. Understanding who is bearing the burden of the crisis and what drives it is crucial for designing policies going forward. Using monthly data from the United States, we find that less-educated women with young children were the most adversely affected during the first nine months of the crisis as schools were kept closed. We estimate that the burden on women of additional childcare accounts for more than 40 percent of the increase in the employment gender gap between April and November 2020; and tt is associated with a GDP loss of 0.36 percent. These results point to the importance of supporting females through financial schemes, training, and investment in childcare and safe measure for school reopening for a speedy economic recovery.

In the outset of the pandemic, most Latin American countries experienced a sharp employment contraction, with large swathes of workers dropping out of the labor force. Although this was followed by a fast rebound, employment still lags its pre-pandemic level and the recovery appears to be uneven across worker types. In our analysis, we use micro-level data from Brazil, Chile, Colombia, Mexico, and Peru—representative of a labor force of over 300 million workers—combined with “real-time” proxies of local economic activity, such as the Google Mobility Index at the metropolitan level. Our analysis shows that the shock hit workers in informal jobs and in small firms the hardest, exacerbating inequality. These workers face more precarious employment conditions and work in sectors that were disproportionately exposed to lockdowns. However, the flexibility of the informal sector—for instance in adjusting hours worked and salaries—appears to be boosting employment in the short-term by absorbing millions of workers who returned to the labor force as sectors gradually re-open. Formal employment, by contrast, experienced a milder contraction but also a more sluggish recovery so far. The presentation will also examine the effectiveness of social programs in mitigating the impact of job losses on household incomes and the risks to the employment recovery that remain going forward.

|

Carlo Pizzinelli Western Hemisphere Department, IMF |

|

Jorge Alvarez Western Hemisphere Department, IMF |